Undervalued Infrastructure Stocks

5 Economic Recovery Value Plays

The infrastructure sector represents one of the most compelling investment opportunities in 2025, combining essential economic function with unprecedented government support and technological transformation. As investors seek undervalued infrastructure stocks 2025 opportunities, a select group of companies trades at significant discounts to intrinsic value while positioning for massive economic recovery benefits.

The Biden Administration's $1.2 trillion Bipartisan Infrastructure Law continues driving historic investments across transportation, energy, and telecommunications infrastructure. Combined with private sector digitalization trends and AI-driven energy demands, the infrastructure landscape presents multiple value creation catalysts that sophisticated investors are beginning to recognize.

This comprehensive analysis examines five exceptional cheap infrastructure stocks trading at substantial discounts to fair value, representing different infrastructure subsectors with unique value propositions and recovery potential. From utility giants managing essential services to technology infrastructure providers enabling digital transformation, these companies offer compelling risk-adjusted returns for patient value investors.

Infrastructure Investment Renaissance: The 2025 Opportunity

Government Spending Catalyst

The Infrastructure Investment and Jobs Act (IIJA) represents the largest federal infrastructure investment since the Interstate Highway System, allocating $695 billion in announced funding across 74,000+ projects nationwide. This sustained government spending creates predictable revenue streams and growth visibility for infrastructure companies positioned to benefit from modernization initiatives.

Key Investment Areas:

Transportation Infrastructure: $284 billion for roads, bridges, and public transit systems

Broadband Expansion: $65 billion for high-speed internet access in underserved areas

Electric Grid Modernization: $73 billion for power grid resilience and clean energy transmission

Water Systems: $55 billion for drinking water and wastewater infrastructure improvements

Private Sector Digitalization

Beyond government investments, private sector digitalization drives unprecedented demand for technology infrastructure. AI workload acceleration, cloud computing expansion, and 5G network deployment create sustained growth opportunities for infrastructure providers across multiple subsectors.

Digital Infrastructure Drivers:

Data Center Demand: AI and cloud computing require massive computational infrastructure

5G Network Rollout: Telecommunications infrastructure expansion enables next-generation connectivity

Smart Grid Technology: Utility infrastructure modernization improves efficiency and reliability

Industrial Automation: Manufacturing and logistics digitization demands robust infrastructure platforms

The Five Value Opportunities

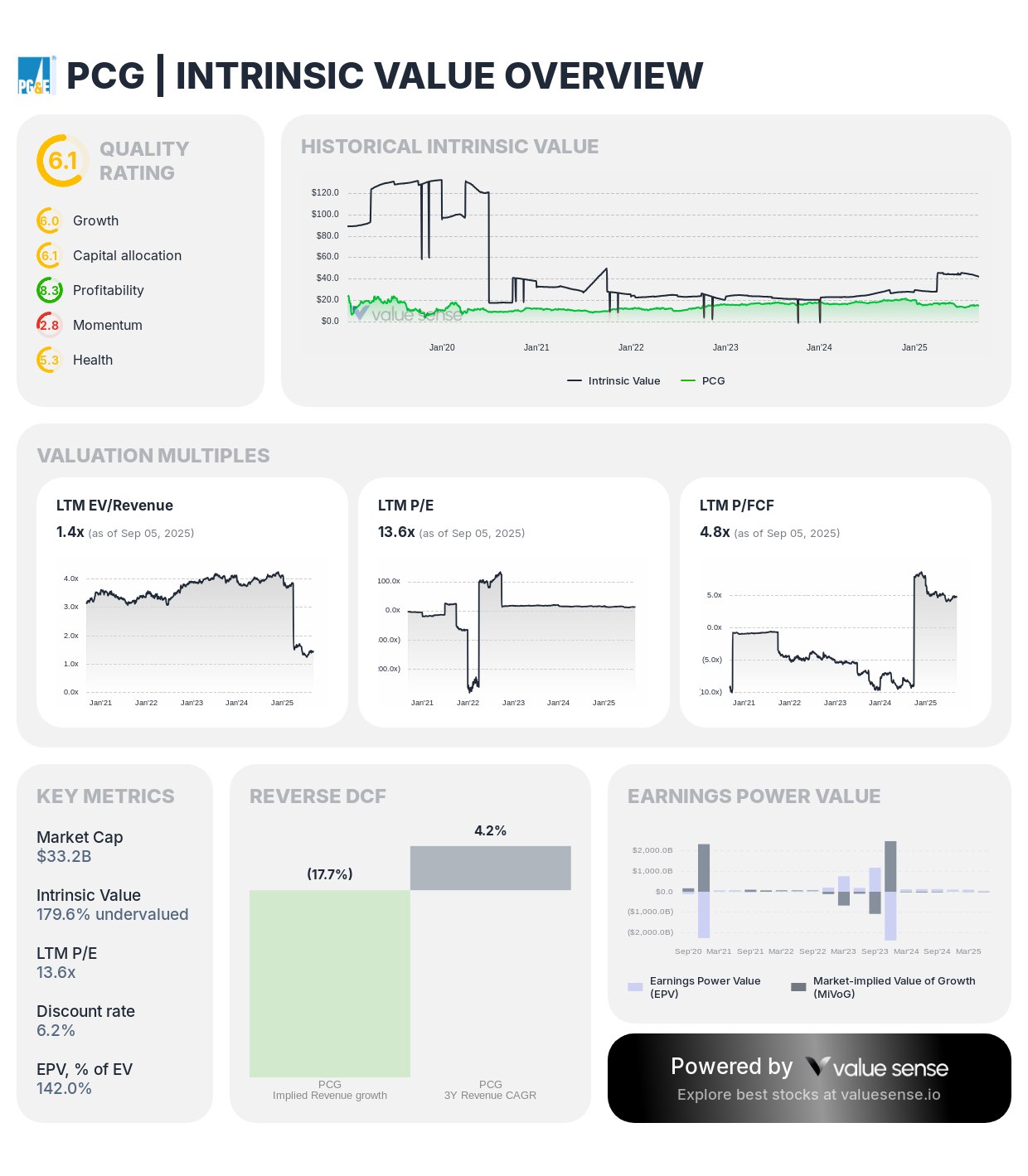

1. Pacific Gas & Electric (PCG): Utility Transformation Value Play

PCG demonstrates exceptional undervaluation at 179.6% below intrinsic value with strong cash generation and quality improvements

Company Profile: Pacific Gas & Electric operates as California's largest utility, serving 16 million customers across Northern and Central California through gas and electric distribution networks.

Value Proposition:

Extreme Undervaluation: 179.6% undervalued relative to intrinsic value

Quality Rating: 6.1/10 with improving operational metrics

Market Cap: $33.2 billion with substantial recovery potential

Cash Generation: $6.93 billion free cash flow with 28.3% FCF margin

Investment Thesis: PCG represents the most undervalued opportunity among infrastructure stocks, trading at a massive discount following bankruptcy resolution and operational improvements. The company's essential utility services, regulatory recovery mechanisms, and wildfire mitigation investments position it for sustained value creation.

Key Catalysts:

Wildfire Risk Reduction: Comprehensive mitigation programs reduce liability exposure

Rate Base Growth: Infrastructure investments generate regulated returns

Clean Energy Transition: California's decarbonization creates growth opportunities

Operational Excellence: Post-bankruptcy focus improves safety and reliability

Financial Strength:

Revenue Growth: 1.3% with stability from regulated operations

ROIC: 9.3% demonstrating effective capital allocation

Free Cash Flow: Exceptional 28.3% margin supports dividend restoration potential

Balance Sheet: Post-bankruptcy capital structure provides financial flexibility

→ PCG fundamentals & intrinsic value analysis

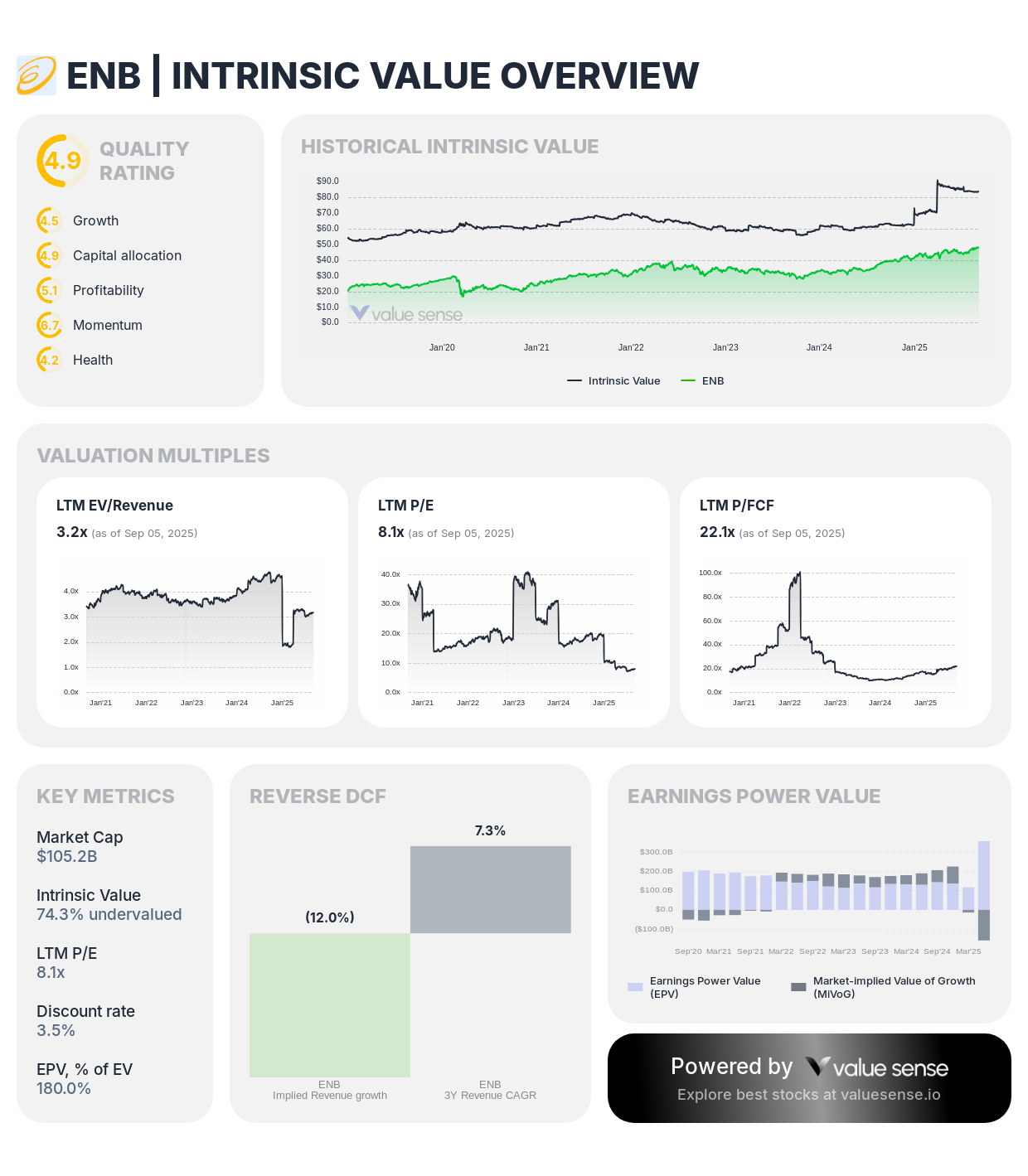

2. Enbridge (ENB): Energy Infrastructure Backbone

Enbridge shows 74.3% undervaluation with exceptional revenue growth and stable cash flows from diversified energy infrastructure

Company Profile: Enbridge operates North America's largest energy infrastructure network, including oil pipelines, natural gas distribution, and renewable power generation across the continent.

Value Proposition:

Significant Undervaluation: 74.3% discount to intrinsic value

Quality Rating: 4.9/10 with strong fundamental characteristics

Market Cap: $105.2 billion reflecting substantial scale

Revenue Growth: Exceptional 48.5% driven by asset expansion

Investment Thesis: ENB provides essential energy transportation and distribution services with regulated utility-like characteristics. The company's diversified energy infrastructure portfolio generates predictable cash flows while participating in North America's energy transition through renewable investments and natural gas expansion.

Key Catalysts:

Pipeline Network Expansion: Strategic acquisitions and organic growth projects

Natural Gas Demand: Increasing demand from power generation and industrial users

Renewable Energy Growth: Wind and solar development complements traditional assets

Dividend Aristocrat: 29-year dividend growth streak demonstrates cash flow reliability

Financial Excellence:

Revenue Scale: $14.9 billion with diversified revenue streams

Cash Generation: $4.76 billion free cash flow with 7.4% margin

ROIC: 6.7% on substantial asset base

Dividend Yield: Attractive income with sustainable payout coverage

→ ENB fundamentals & intrinsic value analysis

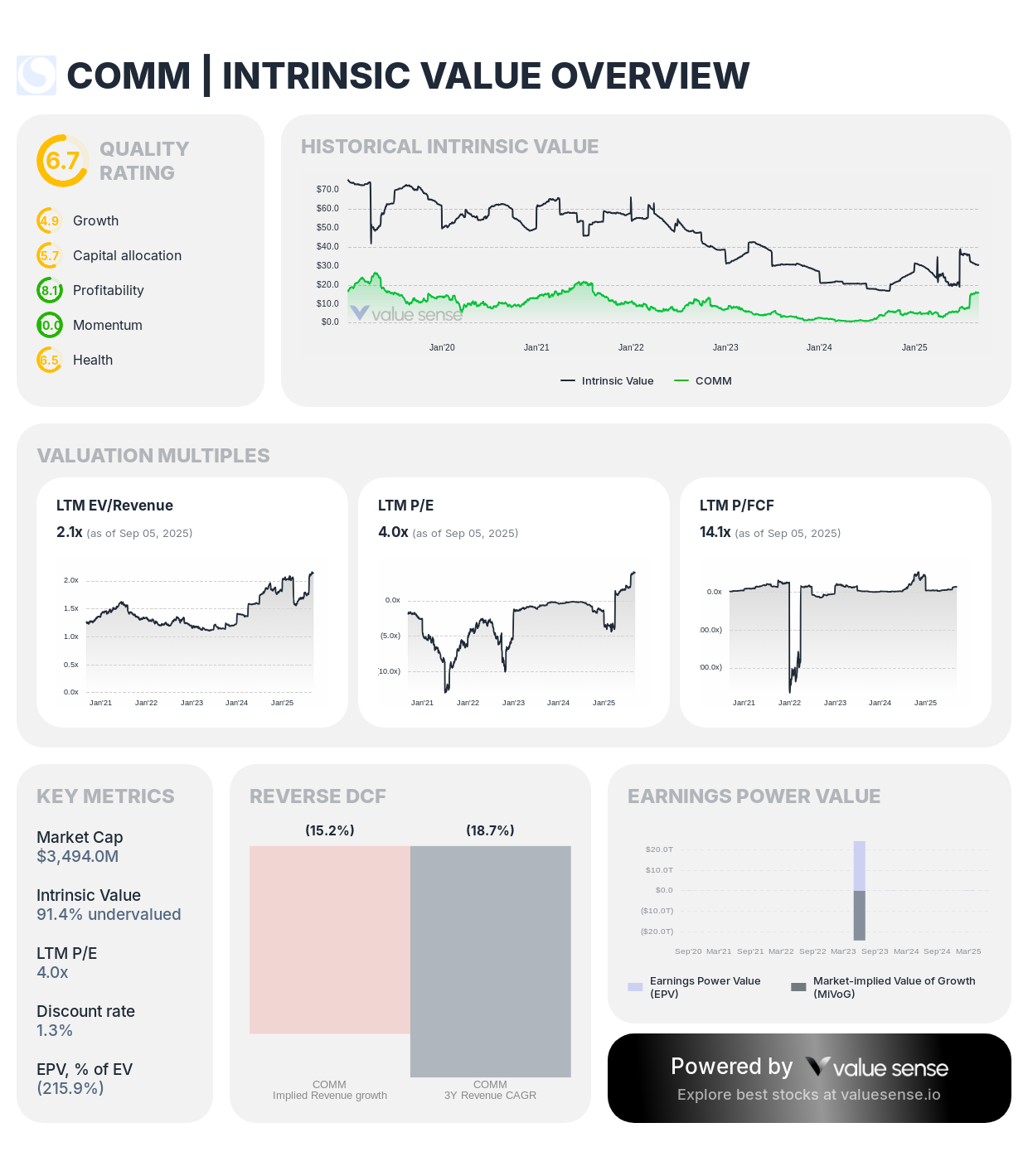

3. CommScope (COMM): Telecommunications Infrastructure Recovery

CommScope trades at 91.4% undervaluation with highest quality rating and positioning for 5G infrastructure buildout recovery

Company Profile: CommScope designs and manufactures infrastructure solutions for communications networks, including wireless, broadband, and enterprise connectivity technologies.

Value Proposition:

Deep Undervaluation: 91.4% below intrinsic value

Highest Quality Rating: 6.7/10 among analyzed companies

Market Cap: $3.49 billion representing recovery opportunity

Revenue Growth: Strong 11.0% expansion

Investment Thesis: COMM represents a classic value recovery play in telecommunications infrastructure. The company's leading position in network equipment and services positions it to benefit from 5G rollout acceleration, broadband expansion initiatives, and enterprise connectivity upgrades.

Key Catalysts:

5G Network Deployment: Accelerating infrastructure investments drive equipment demand

Broadband Infrastructure Act: Government funding supports rural connectivity expansion

Enterprise Digitalization: Corporate network upgrades create sustained demand

Operational Turnaround: Management focuses on profitability improvement and debt reduction

Operational Metrics:

Revenue: $1.39 billion with improving mix

Free Cash Flow: $248 million with 5.2% margin

ROIC: 4.7% with improvement potential

Balance Sheet: Debt reduction priorities support financial stability

→ COMM fundamentals & intrinsic value analysis

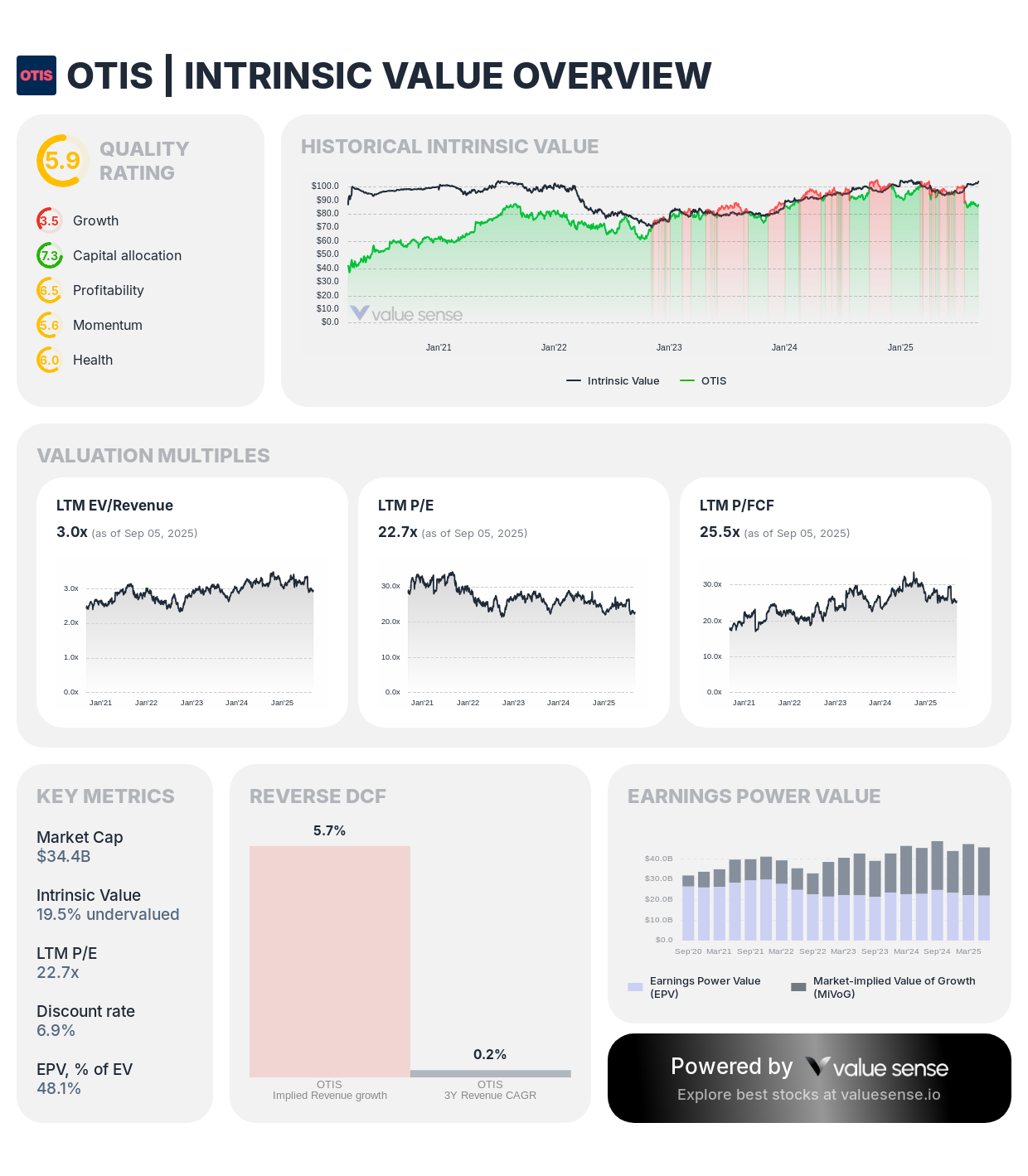

4. Otis Worldwide (OTIS): Vertical Transportation Infrastructure

Otis demonstrates 19.5% undervaluation with exceptional 27.1% ROIC and stable service revenue model

Company Profile: Otis Worldwide manufactures, installs, and services elevators and escalators globally, serving residential, commercial, and infrastructure markets worldwide.

Value Proposition:

Conservative Undervaluation: 19.5% discount to fair value

Quality Rating: 5.9/10 with strong business characteristics

Market Cap: $34.4 billion in established market leader

Exceptional ROIC: 27.1% demonstrates capital efficiency

Investment Thesis: OTIS operates a unique infrastructure business model combining equipment manufacturing with high-margin maintenance services. Urban development trends, building modernization needs, and infrastructure investments drive sustained demand for vertical transportation solutions.

Key Catalysts:

Urbanization Trends: Global urban population growth drives elevator demand

Building Modernization: Aging infrastructure requires upgrades and replacements

Service Revenue Growth: Recurring maintenance contracts provide predictable cash flows

Technology Integration: Smart building systems create premium service opportunities

Financial Quality:

Service Revenue: $3.96 billion from maintenance contracts

Cash Generation: $1.35 billion free cash flow with 9.5% margin

Capital Efficiency: Industry-leading 27.1% ROIC

Revenue Stability: Flat 0.1% growth reflects market maturity but stable demand

→ OTIS fundamentals & intrinsic value analysis

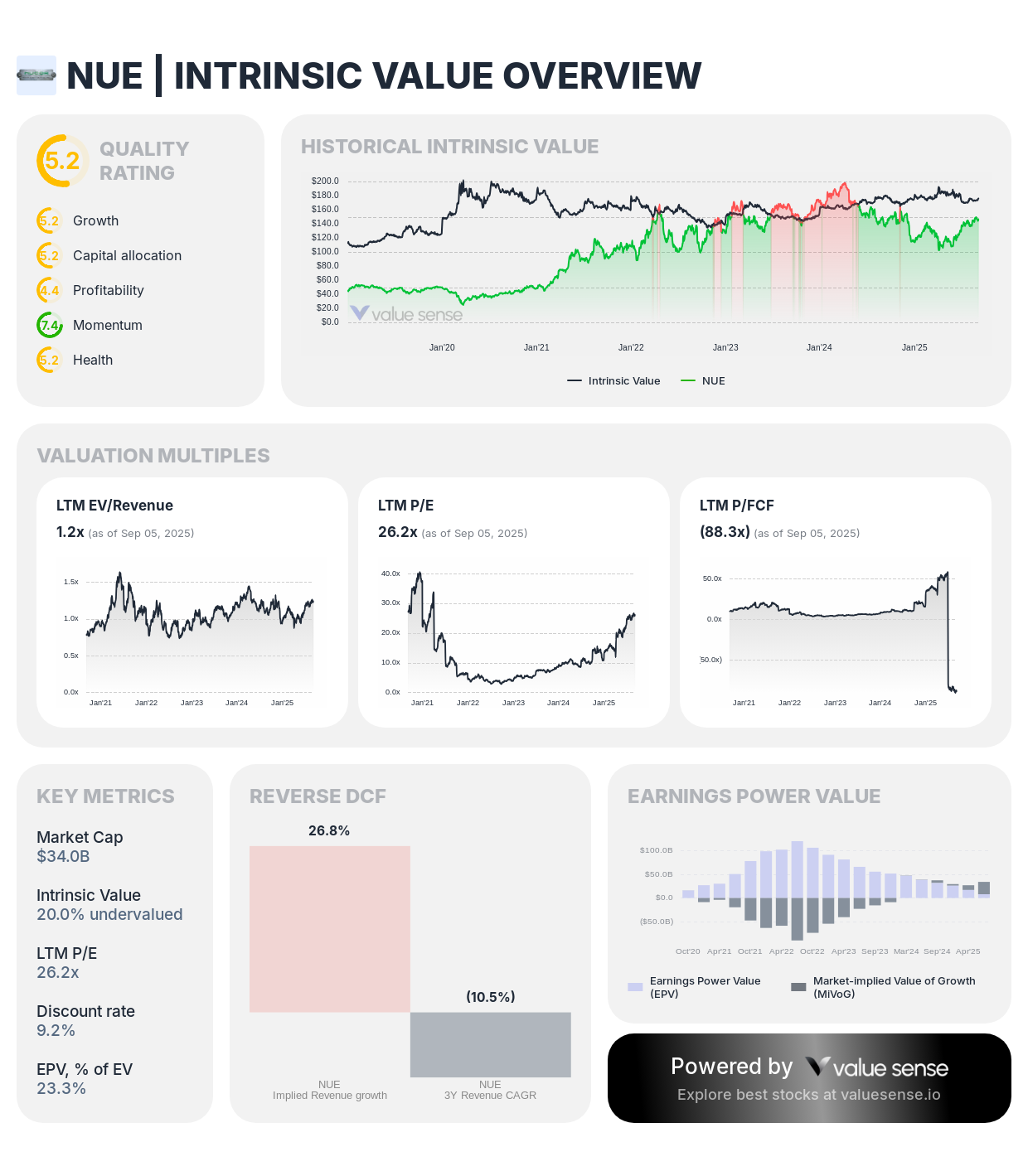

5. Nucor Corporation (NUE): Steel Infrastructure Foundation

Nucor shows 20.0% undervaluation with steady revenue growth and positioning for infrastructure construction demand

Company Profile: Nucor operates as North America's largest steel producer and recycler, manufacturing steel products for construction, automotive, and industrial applications.

Value Proposition:

Modest Undervaluation: 20.0% below intrinsic value

Quality Rating: 5.2/10 with cyclical business characteristics

Market Cap: $34.0 billion in leading steel producer

Revenue Growth: Steady 5.8% expansion

Investment Thesis: NUE provides essential steel products for infrastructure construction while maintaining cost advantages through electric arc furnace technology and scrap steel recycling. Infrastructure spending acceleration and nearshoring trends support sustained steel demand.

Key Catalysts:

Infrastructure Construction: Government spending drives steel demand for bridges, buildings, and transportation

Manufacturing Reshoring: Domestic production trends favor North American steel suppliers

Technology Advantages: Electric arc furnaces provide cost and environmental benefits

Market Leadership: Dominant position enables pricing power and market share maintenance

Operational Considerations:

Revenue: Strong growth from infrastructure and construction demand

Cyclical Nature: Steel pricing volatility affects profitability

Environmental Benefits: Recycling capabilities align with sustainability trends

Capital Allocation: Disciplined investment approach maintains competitive advantages